Project Background and Research Questions

After an Initial secondary research process, I was able to plot out the main questions to answer with another round of secondary research. This is a very thorough research document and could be a bit dry for many, you can click this to directly go to the conclusion of my secondary research

Research Objectives

- Get an estimate on the number of smartphone users in India to select the optimal operating system for the initial product launch.

- What are the statistics for people in India who are already investing?

- Get an estimate on the number of people with bank accounts, PAN cards and Aadhaar cards which will be required for KYC compliance and simplifying the KYC process per government regulations.

- Gain an in-depth understanding of the different investment vehicles available in India.

- What features do current finance apps in the Indian market offer? Who are the direct and indirect competitors?

- What gap remains unaddressed currently?

User Insights and Barriers

Understanding the pain points preventing Indians from investing.

- Is fear of taxation a limiting factor for potential investors?

- Is trust in digital technology or inability to use a digital device a factor?

- Is lack of time a factor preventing investment?

- Is lack of reliable income a barrier to investing?

- Is the language used in the digital space a barrier to investment?

- Is basic literacy a barrier to entry? Is this something within the scope of the current product to address?

- Is perceived risk a factor stopping users from investing?

Findings and what can be addressed in scope

While trying to find credible sources of Information, I found this amazing report based on a survey conducted by Aspero, a SEBI-registered Online Bond Platform Provider (OBPP), and Amaha Health, a mental health organization. The report delves into generational differences, financial goals, risk appetite, and coping mechanisms, uncovering the subtle psychological aspects of wealth accumulation. The key findings hint at intriguing patterns in age-based risk strategies, the evolution of investment portfolios, and gender-based variations in financial aspirations.

And this is the reason why I always thoroughly and exhaustively research before committing to my own primary research. Nearly 80% of my primary research efforts were addressed by this one particular report. This report only helped me slightly in my secondary research though.

You can check the report by entering your details in the page below. You have to give your email address and name in their website to access the pdf report. Its a very good report to read and understand even if you aren’t really interested in my App.

Report by Aspero and Amaha health(opens in the same tab)

The key findings from the report which were relevant to my investment app were as follows :

-

Choice of Investment vehicles varied based on age of the investor.

- Age 21-25 - 60% showed preference for Fixed Deposits and stock markets.

- Age 26-35 - 82.85% showed preference for Mutual Funds.

- Age 36-45 - Even distrubition of funds in low risk and high risk vehicles.

-

The most common motivation for investing based on age groups were as follows :

- Age 21-25 - fund significant life events

- Age 26-45 - saving for emergencies

- Age 36-45 - emergencies and their children’s future expenses

-

Influence of external factors on choice of investment vehicles varied as follows :

- 60% of the participants used online research as their primary method of knowledge seeking.

- 35-40% of the participants used financial advisors and colleagues as their primary method of knowledge seeking.

-

Portfolio check frequency was another finding of the survey

- Most of the respondents checked their portfolio monthly

- Some of the respondents preferred quarterly or sporadic review

- Aggressive investors were more likely to check their portfolio frequently with some even checking it daily

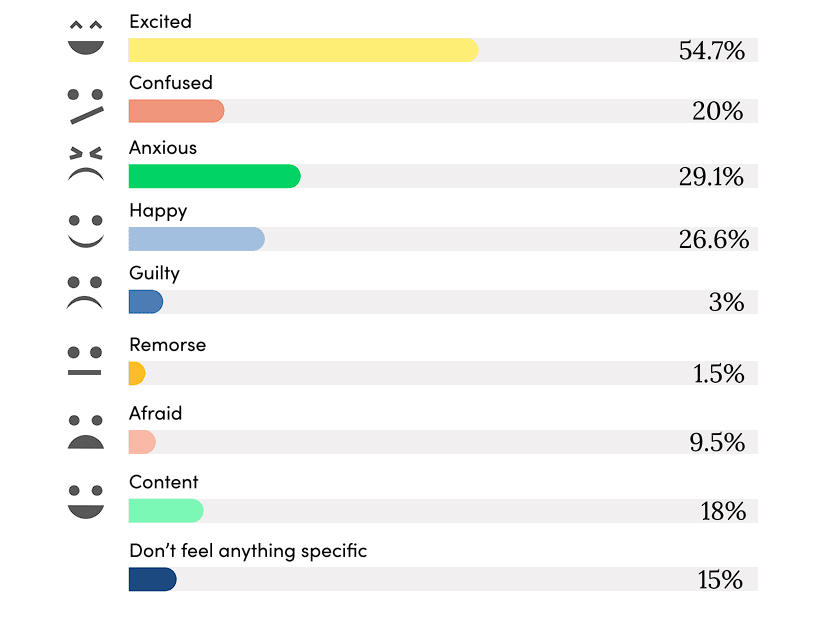

The report also had another very relevant section which tried to address the role of emotions and psychology behind investors:

And here is where I got the most important insight which linked back to Financial Inclusivity and Inclusive Design. My initial research conclusions were validated by this particular Insight :

Lack of knowledge is a significant stressor for investors

And these were respondents who were already investing in some for of investment vehicles. By deduction, lack of knowledge would be an even more significant stressor for novice investors.

Even the report concludes with a similar tone :

The trends identified in the report carry significant implications for the landscape of retail investors in India. The age-based patterns in risk appetite underscore the importance of targeted financial education initiatives, tailoring resources to address the specific concerns and preferences of different age groups. Recognizing the prevalence of moderate risk-taking behavior among the 26-45 age bracket suggests an opportunity for educational programs that address concerns related to market volatility and enhance financial literacy.

The survey methods used by Aspero and Amaha were as follows :

The survey covers inputs from over 300 respondents comprising a mix of salaried professionals, business owners and independent professionals with diverse demographics, income levels, and industry backgrounds.

Since the survey methods addressed a large pool of potential primary research respondents, I only needed to focus on participants who haven’t started investing yet or are very new to investing.

For primary research, I tried to get participants with the criteria for age between 21 and 60, who are either new or have never invested in mutual funds. Since it is a self driven application design, budget constraints meant that I had to depend a lot more on the secondary research. I used online surveys, hallway user surveys, etc. to validate the hypothesis from my secondary research.

Research Insights Which Guided my Design Decisions and Scope Definition

From the primary and secondary research I distilled these points around which I could use to guide my designs.

- As of December 2013, Android has a 95%+ market share of devices in India

- 80 million people unique investors in India, out of which 40 million use mutual funds as their preferred device( according to NSE in September 2023), less than 10% of Indians.

- As of Feb 2023, 482 million bank accounts in India, 610 million pan card holders, 1.3 billion aadhar card holders.

- Fixed Deposits and Savings Accounts remain the most used investment vehicles in India largely due to being perceived as safe and stable investments.

- Lack of time and awareness is another major factor among those who aren’t investing.

From competitors, I noticed a few major problems one which goes completely unaddressed and the others which are addressed but not completely

- Lack of language options. According to Forbes, only 30% of Indians understand English. By not offering other language options, you lose out on 70% of the population, a big blow to inclusivity.

- The applications assume your proficiency and knowledge. There’s no handholding. There’s no guidance. INDMoney is the only App which has a built in learning module at the time of research (December 2023), but its obscured away under your profile. Not easy for a new investor to know such a module exists.

- There’s an incredible information overload the moment you get into these apps and you cannot even try the app without registering and while using the app, there’s a regular user flow disturbance by pushing for KYC completion which was very jarring.

- Zerodha Kite had a demo but it was a stock trading app. The mutual fund app Zerodha Coin had no such demo options. Also the whole Zerodha environment was a bit confusing. The also have Zerodha Varsity app for learning. It’s very inconvenient to make a potential user install 3 different applications.

- From a UI design perspective, most of the competitors were very well made and looked very pleasant. Helped me a lot in understanding and plotting userflows since the Mutual Funds topic is heavily regulated by the govt. I realized that some User Flows had very less room for change and were heavily regulated.

Outside of the major gaps, I identified some minor gaps based on the my findings and the Aspero and Amaha report:

- Achieving goals was the single most important reason why people invest in mutual funds.

- Even if the SIP minimum amount is decreased to Rs 250, financial literacy will remain a significant limiting factor in India which remains unaddressed. There’s very large untapped potential here.

- Portfolio management is an area where signficant USP can be created with the help of AI.

There were other significant research findings which were relevant, but are strictly outside of the scope of the product implementation :

- The lack of awareness of the existence of Investments like Mutual Funds

- The perceived risk of investments being so high that they don’t even try to understand it

- The perceived barrier of entry with respect to financial knowledge is very high.

- Many investors report that they have had bad past experience with mutual funds due to their lack of knowledge and being made to sign up for bad products like ULIPs

Working on these points are outside of the scope of the mutual fund app. This needs marketing, education and other external campaigns to address these issues.